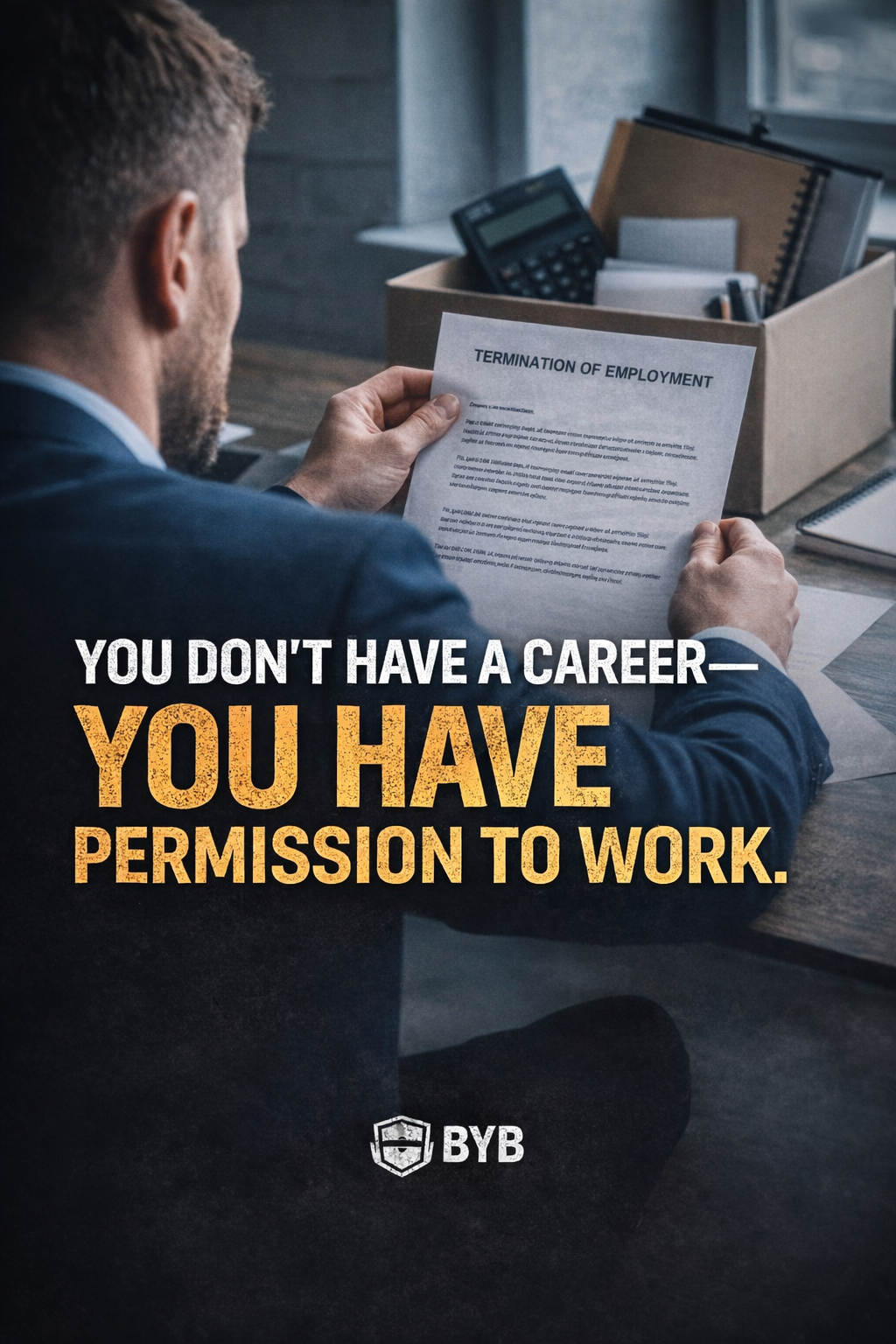

You’re not an employee with job security. You’re someone who needs permission to pay rent.

Every month, you wait for someone else to decide whether you survive. You call that “stable employment.” What it actually is: financial dependence with a direct deposit schedule.

The company can revoke your permission tomorrow. Restructuring. Downsizing. “Strategic realignment.” You don’t control when the money stops. You just convinced yourself that not controlling it means it’s safer.

Here’s what stings: for most people, you’re not building wealth on that salary. You’re funding survival.

Your 5% annual raise isn’t progress. It’s you losing ground to inflation slowly enough that you don’t panic and do something about it. Meanwhile, the people who own equity in the company you work for are compounding wealth from systems you help build.

You’re not choosing safety. You’re choosing to let someone else control whether you survive. And calling that wisdom.

This is job security vs entrepreneurship. One is renting permission to work. The other is owning outcomes. One caps your ceiling and calls it responsible. The other removes the cap but requires you to handle chaos.

Most people choose the cap. Then spend thirty years wondering why wealth never materialized.

Quick Summary: Job Security vs Entrepreneurship — The Financial Choice Most People Get Wrong

Three financial structures determine your outcome:

- Employee — Capped income, zero leverage, comfort without wealth

- Investor — Compound growth, but requires capital most salaries don’t provide

- Entrepreneur — Unlimited upside, brutal variance, chaos for 3-5 years

Core reality: Salary alone = survival income. Ownership = wealth engine. Most people need salary as the base and ownership to break the ceiling.

The trap: optimizing for one while ignoring the other.

You Don’t Have Security — You Have Permission

Your employment contract isn’t security. It’s permission to work that expires when convenient for the company.

Ten years building expertise in one company’s systems. They pivot. Your skills don’t transfer. You’re not employable elsewhere because you optimized for internal processes instead of market-valuable capabilities. You thought you were building a career. You built dependency.

Salary Has a Ceiling You Will Never Break

The company budgeted $120K for your role. You negotiate within that range, not outside it. Generate $2 million in value, get a $10K raise. The difference is profit — captured by equity owners, not salary employees.

This isn’t exploitation. It’s how companies function. Employees exchange time for predictable income. Owners capture value from systems. One has a ceiling. One scales exponentially.

The Employee Structure: Capped Income, Limited Leverage

Time for money. Linear exchange. Work more hours, make marginally more money. Stop working, money stops immediately.

Raises are incremental. $50K becomes $90K over twenty years. After inflation, that $90K buys what $55K bought when you started. You worked two decades to maintain the same purchasing power.

For most households, salary covers expenses but doesn’t build meaningful wealth. If you expect it to without ownership, you’ll work forty years and retire with limited financial options compared to those who built equity early.

Why Salary Optimization Is a Trap

You’re negotiating for a 10% raise. $80K to $88K. Feels like progress.

Meanwhile, the founder whose company you work for just did a Series B at a $200M valuation. Their 30% equity stake is now worth $60 million on paper. Your $8K raise doesn’t even register as rounding error in that equation.

You’re playing a different game. They’re building equity that scales. You’re trading time for incremental adjustments that inflation erases.

This isn’t a moral judgment. It’s a structural reality. Salary has a ceiling. Equity doesn’t.

Most employees never realize they’re optimizing within a system designed to cap their upside while extracting maximum value from their labor. By the time they figure it out, they’re forty-five with obligations that make transition impossible.

The Investor Structure: Compound Growth You Can’t Access

Capital compounds. $10K invested at 8% annual returns becomes $46K in twenty years. Exponential growth, not linear.

The math works. The problem: you can’t deploy it.

You need capital to invest. Salary barely covers rent, student loans, childcare, and the lifestyle you convinced yourself was necessary. There’s nothing left to deploy.

This is the investor’s trap for employees. The strategy works in theory. In practice, salary doesn’t leave room for meaningful capital accumulation. You’re stuck trading time for money that disappears before you can convert it into assets that compound.

Why “Just Invest” Advice Fails for Most Employees

Financial advisors tell you to invest 15% of income. On $70K salary, that’s $10,500 per year or $875 per month.

Sounds reasonable until you subtract typical urban living costs: rent ($1,800), student loans ($400), car payment ($350), insurance ($200), groceries ($600), and the occasional emergency that drains whatever you managed to save.

The 15% doesn’t exist. What exists is $200 per month deposited into an index fund that will compound into a retirement nest egg that covers maybe ten years of expenses if you’re lucky and don’t encounter medical catastrophes.

For more on building passive income while employed, the core challenge is capital access — and salary rarely provides enough margin to deploy capital at scale.

You need equity ownership. Not just stock market equity. Ownership in businesses, real estate, systems that generate cash flow regardless of whether you’re actively working.

The Entrepreneur Structure: Variance Most People Can’t Survive

Build systems that operate independent of your time. Year one: -$30K. Year three: break even. Year five: $200K. Year ten: $1M+.

High variance. Most businesses collapse in the first year — not because the idea failed, but because founders couldn’t survive the financial and psychological chaos long enough for systems to generate positive returns.

This works if you tolerate losing money for two to four years while building leverage. If you can’t, you’ll quit before compounding kicks in.

Why Most People Fail at Entrepreneurship

They quit employment with no customers, no revenue, and six months of savings. They “follow their passion” into a market that doesn’t care. They optimize for lifestyle freedom before building systems that generate reliable cash flow.

Smart transition: Build while employed. Prove market demand. Scale revenue to 50-100% of salary. Then quit with reduced risk and validated systems. Quitting first means building under financial pressure — desperation makes bad decisions.

Why You Stay Stuck (And Why You Know It)

You’re not staying employed because it’s optimal. You’re staying because you’re terrified of variance.

Losing a $70K salary feels catastrophic. Never making $200K feels like missed potential, not loss. You overweight the pain of losing what you have versus the opportunity cost of what you’ll never build.

Loss aversion isn’t irrational. It’s evolutionary. It’s also the reason you’ll stay financially capped for decades.

The Conditioning That Keeps You Dependent

Get good grades. Get a degree. Get a job. Get promoted. Repeat for forty years. Retire with a pension that doesn’t exist anymore.

Nobody taught you to build systems. Nobody explained that salary caps wealth creation by design. The conventional path optimizes for employment stability — which benefits employers who need predictable, skilled labor.

By the time you realize the structural limitations, you’re thirty-five with a mortgage, two kids, and financial obligations that make risk intolerable. You’re locked in.

Most corporate systems reward compliance and predictability over risk-taking and ownership. This isn’t conspiracy — it’s incentive alignment. Companies need stable workforces. Employees who build ownership optionality become harder to retain. That’s why companies structure retention incentives: promotion ladders, vesting schedules, benefits packages, and golden handcuffs designed to make leaving expensive.

Once salary covers survival plus minor comfort, giving it up feels impossible. Not because employment is objectively better. Because losing guaranteed income triggers panic even when keeping it as your only strategy almost guarantees you’ll never build significant wealth.

You’re choosing dependence and calling it responsibility. That’s not wisdom. That’s Stockholm syndrome with a 401(k).

Salary vs Ownership: The Binary Choice You’re Avoiding

You don’t have to quit your job tomorrow. You have to stop expecting salary to build wealth.

Salary = time exchanged for capped, predictable income.

Ownership = equity in assets and systems that compound independent of your time.

Four Paths to Ownership While Employed

1. Index Fund Equity

Own fractional stakes in 500+ companies through low-cost index funds. According to S&P Dow Jones Indices, the S&P 500 has averaged approximately 10% annual returns over long periods. $500/month invested over twenty years at 10% = $380K. Not retirement wealth, but a foundation.

2. Real Estate Ownership

Cash-flowing rental properties. Buy with leverage (mortgage), tenants cover debt service, you own appreciating asset. One property becomes five over fifteen years through equity buildup and reinvestment.

3. Side Business Systems

Build while employed. SaaS product, consulting service, e-commerce store. Start small, prove revenue, scale until business income matches salary. Then transition or keep both.

4. Equity Compensation

Negotiate ownership, not just salary. Stock options, profit sharing, equity grants. If the company you’re building value for won’t give you equity, find one that will or build your own.

Employment provides the base. Ownership builds wealth. Salary alone keeps you stuck. Ownership alone is unstable early on. You need both.

Stop Romanticizing Entrepreneurship (And Employment)

The Entrepreneurship Delusion

Don’t quit to “follow your passion” or “be your own boss.” That’s how failures start.

Drain savings. Quit stable income. Build with no customers, no validated demand, no proof the market cares. Six months later: broke, demoralized, LinkedIn post about “lessons learned” that translates to “I failed because I had no idea what I was doing.”

Build while employed. Prove demand. Scale revenue. Quit when keeping the job becomes the bottleneck, not when you’re tired of your manager.

The Employment Delusion

Employment isn’t inherently bad. It’s bad when you expect it to do something it was never designed to do: build wealth.

Employment provides predictable income, benefits, structure, skill development, network access. These things have value. They don’t compound into generational wealth, but they’re not useless.

The mistake is thinking you can get rich on salary. You can’t. Salary funds survival and provides capital to deploy into ownership. That’s its function.

If you optimize employment correctly — high income, low expenses, deploy surplus into equity ownership — you can build wealth while maintaining income stability. Most people do neither. They optimize for lifestyle inflation instead of capital deployment.

Permission to Work Expires When It’s No Longer Profitable

The social contract is dead. Pensions evaporated. Loyalty is unrewarded. According to Bureau of Labor Statistics data, median employee tenure is approximately four years. Companies lay off profitable divisions to optimize quarterly earnings for shareholders.

The “security” you’re optimizing for doesn’t exist. What you call job security is permission to work. That permission expires when:

- Your role gets automated by AI or software

- Your salary becomes too expensive relative to market alternatives

- The company pivots and your expertise becomes irrelevant

- Shareholders demand cost optimization and HR finds your name on the spreadsheet

You’re not building toward a secure retirement. You’re renting income from an entity that will terminate the lease the moment it serves their interest.

The Only Real Security: Creating Value Markets Pay For

If you can generate value people or companies will pay for, you’re antifragile. Lose your job, find another or start your own. Skills transfer. Ownership transfers. Dependence on one employer does not.

The goal isn’t to quit employment. The goal is to make employment optional by owning assets that generate income whether you work or not.

Employment as your only income source: fragile. One termination away from financial crisis.

Employment + index funds: more stable, but still capped by salary limitations.

Employment + real estate + side business: antifragile. Multiple income streams, compounding equity, optionality.

If one company controls whether you survive, you’re not secure. You’re dependent. And dependence pretending to be security is the most dangerous financial position possible.

The Wealth System You’re Not Playing

There’s a hierarchy most employees never see:

Tier 1: Laborers

Trade time for hourly wages. Zero leverage. Income stops when labor stops.

Tier 2: Salaried Employees

Trade time for predictable income and benefits. Capped upside. Income stops when employment stops.

Tier 3: Equity Owners (Passive)

Own shares in businesses, real estate, funds. Income continues regardless of active labor. Compounds over time.

Tier 4: Equity Owners (Active)

Build and own businesses, real estate portfolios, operating companies. Control value creation. Capture majority of upside.

Most people are Tier 1 or 2. They think they’re building careers. They’re funding someone else’s Tier 4 wealth accumulation.

If you don’t own something that compounds, you’re not a player in the wealth system. You’re an input the system consumes.

The gap between Tier 2 (salaried employee) and Tier 3 (equity owner) is the difference between comfortable poverty and financial independence. The gap between Tier 3 and Tier 4 is the difference between financial independence and generational wealth.

You can move between tiers. But you have to understand which tier you’re in and what’s required to move up. Most people optimize within Tier 2 for forty years and wonder why wealth never appeared.

You’re not going to salary-negotiate your way to Tier 4. You’re going to own your way there.

Should You Quit Your Job? (Probably Not Yet)

Don’t quit to start a business. Quit because the business already works and employment is now the constraint.

Build while employed:

- Nights and weekends for 6-12 months

- Validate market demand (customers willing to pay)

- Prove unit economics work (revenue > cost to acquire + deliver)

- Scale to $3K-5K monthly revenue

- When business income hits 50-100% of salary, evaluate transition

If you quit before proving the model works, you’re not being bold. You’re being reckless.

Entrepreneurship isn’t passive income. It’s trading predictability for leverage. Year one and two: more work than employment, not less. Customer complaints. Cash flow fires. Hiring mistakes. Operational chaos.

If you want passive, buy index funds and rental real estate. If you want leverage and you’ll manage chaos for three to five years until systems stabilize, build a business.

But don’t quit employment until the business proves it can replace employment income. Too many founders die in the gap between quitting and revenue.

You Can Be Employed and Still Own Equity

Employment is not wrong. Dependence without ownership is.

There’s nothing inherently bad about working for a company. Employment provides income stability, skill development, network access, health insurance, and structure. These things have value. The mistake is expecting employment to do something it was never designed to do: build generational wealth.

The problem isn’t that you have a job. The problem is that you only have a job — and you expect that singular income source to fund both survival and wealth creation simultaneously. It can’t. Salary covers expenses. Ownership builds wealth.

You can have both. Use salary as the base. Deploy surplus capital and time into equity ownership. Most people choose one or the other and fail.

The optimal path: Maintain employment income while systematically building ownership in assets that compound.

Index funds. Rental real estate. Side businesses. Equity compensation. These aren’t alternatives to employment. They’re how you use employment income to escape employment dependence.

If you only have salary, you’re not building wealth. You’re renting survival from someone who can evict you whenever it’s convenient.

But if you have salary + ownership, you’re using the stability of predictable income to build leverage that eventually makes income optional.

That’s the goal. Not to quit your job and struggle. To build enough ownership that your job becomes a choice, not a necessity.

When work is optional, you’ve won. When work is mandatory, you’re still renting permission.

Frequently Asked Questions About Job Security vs Entrepreneurship

Is job security really dead? The traditional employment contract — lifetime loyalty rewarded with pensions and stability — is gone. Average employee tenure is four years. Companies optimize for shareholder returns, not employee welfare. Layoffs happen during record profit years. The “security” employees optimize for is permission to work, not guaranteed income. That permission expires when automation, cost optimization, or strategic pivots make your role redundant.

Should I quit my job to start a business? Don’t quit to start. Build while employed, prove market demand, scale revenue to 50-100% of your salary, then evaluate transition. Quitting with no customers and no proof is how most failures begin. Use employment as the financial base while building systems that could eventually replace it. Quit when the business works and employment becomes the constraint — not when you’re frustrated or bored.

What’s the real difference between salary and ownership? Salary trades time for capped, predictable income. Stop working, income stops immediately. Ownership captures value from systems that operate independent of your time. Employees get annual raises. Owners capture exponential returns from leverage and compounding. One has a ceiling designed into the compensation structure. One scales without limits if systems are built correctly.

Can you actually build wealth on a salary? Salary alone will not build wealth — it covers expenses and provides stability. But you can build wealth while employed by owning equity: index funds, rental real estate, side businesses, equity compensation. Employment provides the base and capital source. Ownership is where wealth compounds. You need both. Salary without ownership keeps you capped. Ownership without stable income creates unsustainable variance early on.

How long does it take to transition from employee to entrepreneur? Build while employed for 12-36 months depending on business model complexity. Validate demand in months 1-6. Prove unit economics in months 6-12. Scale to meaningful revenue ($3K-5K monthly) in months 12-24. Transition when business income consistently hits 50-100% of salary and growth trajectory is clear. Most successful entrepreneurs didn’t quit first — they proved the model worked while employed, then transitioned strategically with reduced risk.

Why do most people never build wealth despite working for decades? They optimize within a system designed to cap their upside. Salary has a ceiling. Lifestyle inflation consumes raises. No surplus capital gets deployed into ownership. They trade time for money for forty years, expecting wealth to appear from incremental salary increases that barely keep pace with inflation. Wealth comes from owning assets that compound — not from trading time for capped income. Most employees never make that structural shift.

Leave a Reply